Are you Getting a Fixed-rate mortgage? Some things to consider!

October 12, 2018 | Posted by: Keith Leighton

Are you Getting a Fixed-rate mortgage? Some things to consider!

Are you considering a 25-year amortization or 30 years? Insured or Uninsured? With an A Lender or B Lender? These are just a few of the questions people have to decide on when they are pursuing a mortgage. But the biggest question of all: Fixed Rate or Variable Rate?

With the instability of the market, and the Bank of Canada’s continuous rate hikes, many people now are flocking towards a fixed rate mortgage over a variable rate. What this means is that they are choosing to essentially “lock in” at a rate for the term of their mortgage (5 years, 10 years, 1 year…you name it). Now there are benefits to this…but there are also disadvantages too.

For example, did you know that 60% of people will break their mortgage by 36 months into a 5 year term? Whether it’s due to career changes, deciding to have kids, wanting to refinance, or another reason entirely, 60% of mortgage holders will break it.

And just like any other contract out there, if you break it, there is a penalty associated with it. However, there is a way to avoid paying more than is necessary. This applies directly to a fixed rate mortgage and we can help you decide what lenders you should go with.

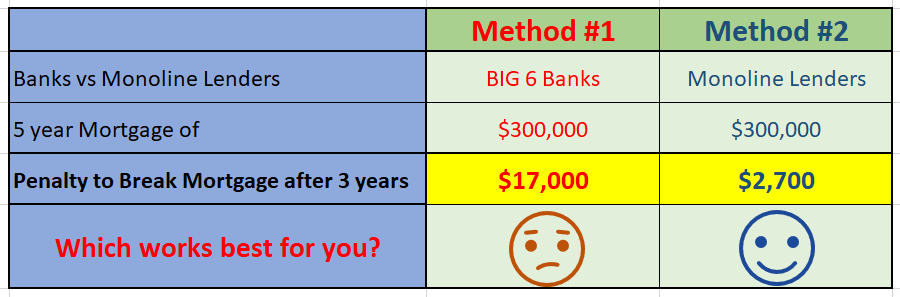

If you have a FIXED RATE MORTGAGE: There are two ways your penalty will be calculated.

Method #1. If you are funded by one of the Big 6 Banks (ex. Scotia, TD, etc.) or some Credit Unions, your penalty will be based on the bank of Canada Posted Rate (Posted Rate Method) To give you an example:

With this method, the Bank of Canada 5 year posted rate is used to calculate the penalty. Under this method, let’s assume that they were given a 2% discount at their bank thus giving us these numbers:

Bank of Canada Posted Rate for 5-year term: 5.59% Bank Discount given: 2% (estimated amount given*) Contract Rate: 3.59%

Exiting at the 2-year mark leaves 3 years left. For a 3-year term, the lenders posted rate. 3 year posted rate=3.69% less your discount of 2% gives you 1.44%. From there, the interest rate differential is calculated.

Contract Rate: 3.59% LESS 3-year term rate MINUS discount given: 1.69% IRD Difference = 1.9% MULTIPLE that by 3 years (term remaining) 5.07% of your mortgage balance remaining. = 5.7%

For that mortgage $300,000 mortgage, that gives a penalty of $17,100. YIKES!

Now let’s look at the other method (one used by most monoline lenders)

Method #2: This method uses the lender published rates, which are much more in tune with what you will see on lender websites (and are “generally” much more reasonable). Here is the breakdown using this method:

Rate when you initially signed: 3.24% Published Rate: 3.34% Time left on contract: 3 years

To calculate the IRD on the remaining term left in the mortgage, the broker would do as follows:

Rate when you initially signed: 3.24% LESS Published Rate: 3.54% =0.30% IRD MULTIPLY that by 3 years (term remaining) 0.90% of your mortgage balance

That would mean that you would have a penalty of $2,700 on a $300,000 mortgage.

Let’s Compare:

That’s a HUGE difference in numbers, just by choosing to go with a different lender! Knowing what you know about fixed rate mortgages now, let a Dominion Lending Centres Ideal Mortgage mortgage broker help you make the RIGHT choice for your lender. We are here to help and guide you through the mortgage process from pre-approval onward!